Synthetic Gypsum Market Overview Size, Share & Trends Analysis, 2024- 2032

REPORT DETAILS

Market Statistics

Market Overview

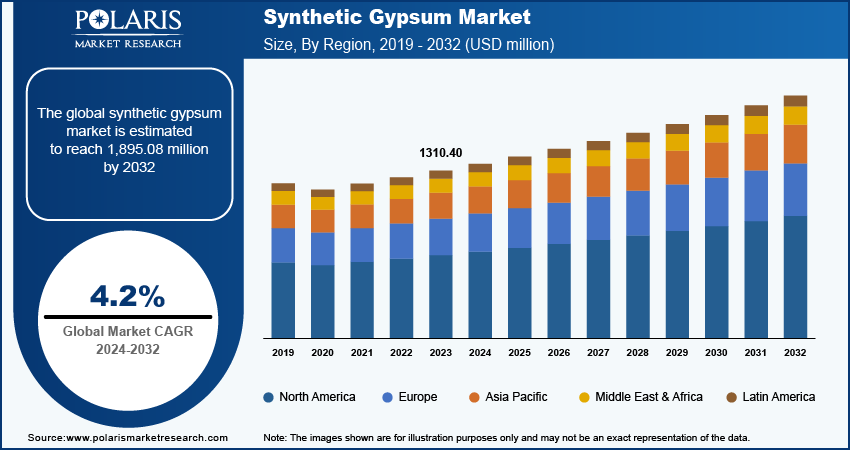

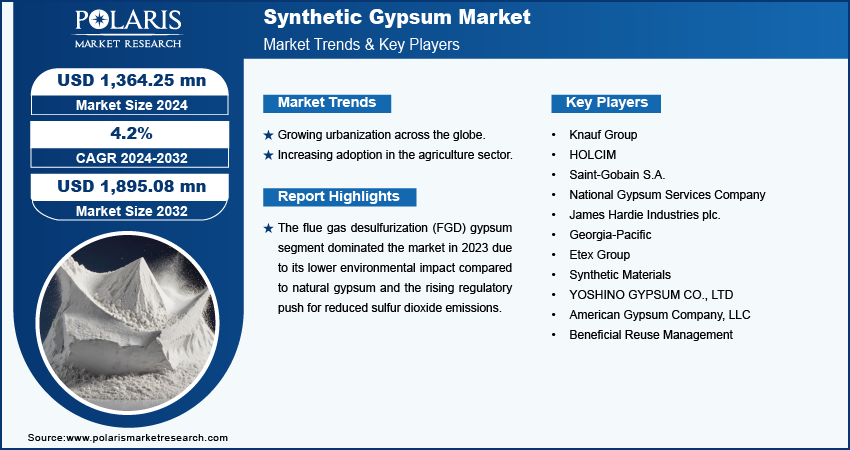

The global synthetic gypsum market size was valued at USD 1,310.40 million in 2023. The market is projected to grow from USD 1,364.25 million in 2024 to USD 1,895.08 million by 2032, exhibiting a CAGR of 4.2% during 2024–2032.

Synthetic gypsum is an artificial alternative to natural gypsum. It is generally produced as a by-product of industrial processes, particularly through flue gas desulfurization (FGD) in coal-fired power plants. Synthetic gypsum is majorly composed of calcium sulfate dihydrate and has similar properties like natural gypsum. This makes it suitable for various applications in construction, agriculture, and other industries.

The growing urbanization across the globe drives the synthetic gypsum market growth. According to data published by the United Nations, 68% of the world's population is projected to live in urban areas by 2050. Urbanization leads to a rise in construction projects, including residential, commercial, and infrastructure developments. Synthetic gypsum is a key ingredient in drywall and plaster products, which are essential in these projects. Therefore, as urbanization rises, the demand for synthetic gypsum increases.

Rising environmental regulations worldwide are projected to propel the global synthetic gypsum market. Environmental regulations often emphasize sustainability and reducing the environmental footprint of construction materials. Synthetic gypsum is considered more sustainable than natural gypsum. It helps recycle waste products, thereby aligning with green building standards and certifications, which makes it a preferred choice in regulated markets.

Source: Polaris Market Research Analysis

To Understand More About this Research: Download Sample Report

The synthetic gypsum market is driven by increasing investments in research and development activities. R&D investments often lead to the development of new and improved formulations of synthetic gypsum. Innovations enhance the performance characteristics of synthetic gypsum, such as its durability, fire resistance, or ease of application. These advancements make synthetic gypsum more attractive to potential consumers, increasing its demand in several industries, such as the construction industry.

Drivers and Opportunities

Rising Per Capita Income Worldwide

There is a rising per capita income across the world. For instance, GDP per capita growth in the world was reported at 1.7798 % in 2023. Homeowners with increased disposable income are spending on home renovations and remodeling projects to upgrade their properties. Synthetic gypsum, used in drywall and other interior finishes, becomes a preferred material in these projects due to its quality and performance characteristics, thereby boosting its demand. Thus, the rising per capita income fuels the growth of the synthetic gypsum market.

Increasing Adoption in Agriculture Sector

Synthetic gypsum is gaining attention in the agriculture sector for its benefits in enhancing soil health and structure. It improves soil tilth by breaking up compacted layers, which enhances root growth and water infiltration, leading to increased crop yields and maintaining soil fertility. This encourages farmers to adopt and involve synthetic gypsum in their farming practices. Thus, increasing adoption of Synthetic gypsum in agricultural practices is expected to offer lucrative opportunities for the market during the forecast period.

Source: Polaris Market Research Analysis

Get Full Segment-Level Forecasts & Insights: Download Sample Report

Segment Insights

Type-Based Insights

Based on type, the global synthetic gypsum market is segmented into flue gas desulfurization (FGD) gypsum, fluorogypsum, phosphogypsum, titanogypsum, and others. The flue gas desulfurization (FGD) gypsum segment dominated the market in 2023. The regulatory push for reduced sulfur dioxide emissions has led to increased implementation of FGD systems. These systems help comply with environmental regulations and produce a high volume of FGD gypsum utilized in construction applications such as drywall and plasterboard. The material's properties, including its suitability for various building applications and its lower environmental impact compared to natural gypsum, contributed to its dominant position in the market.

Application-Based Insights

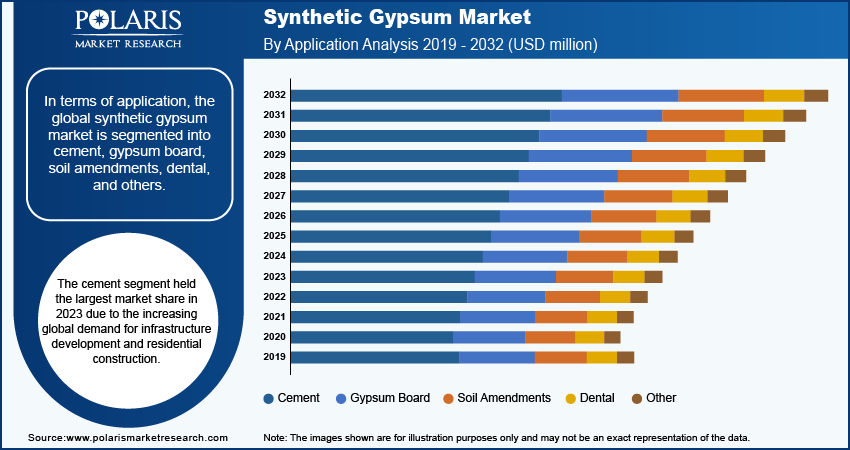

In terms of application, the global synthetic gypsum market is segmented into cement, gypsum board, soil amendments, dental, and others. The cement segment held the largest market share in 2023 due to the increasing global demand for infrastructure development and residential construction. Cement manufacturers value synthetic gypsum for its consistent quality and cost-effectiveness compared to natural gypsum. Additionally, stringent environmental regulations that mandate the reduction of carbon emissions have encouraged cement producers to utilize by-products from industrial processes, such as synthetic gypsum, which reduces the need for natural raw materials and helps in managing industrial waste.

The soil amendments segment is expected to grow at a robust pace in the coming years, owing to the increasing focus on sustainable agriculture and the need to improve soil health and crop yields. Synthetic gypsum offers significant benefits as a soil conditioner, including reducing soil erosion, improving water infiltration, and providing essential calcium and sulfur nutrients to plants. The rise in organic farming and the growing awareness of soil management practices are driving the adoption of synthetic gypsum in agricultural applications. Additionally, the ability of synthetic gypsum to repair sodic soils further supports its expanding use in agriculture.

Source: Polaris Market Research Analysis

Need Granular Data Across All Market Segments? Request Customization

Regional Insights

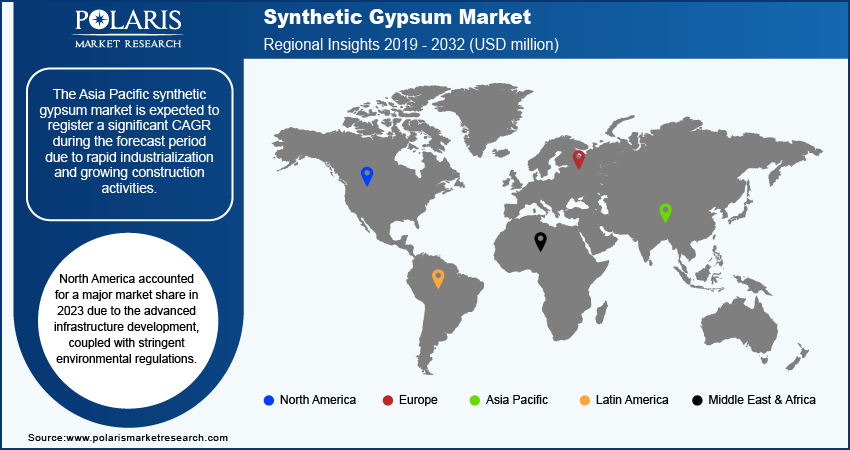

By region, the study provides the synthetic gypsum market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America accounted for a major market share in 2023 due to the extensive use of this material in construction and industrial applications. The region's advanced infrastructure development, coupled with stringent environmental regulations that encourage the use of by-products from flue-gas desulfurization processes, has fueled demand of synthetic gypsum. The US, as the dominant country in this region, has led the way with significant investments in construction and renovation projects. Additionally, the presence of major drywall manufacturers such as American Gypsum Company, LLC; Etex Group; and HOLCIM contributes to North America's leading position in the market.

The Asia Pacific synthetic gypsum market is expected to register a significant CAGR during the forecast period due to rapid industrialization and growing construction activities. Countries such as China and India are driving this growth with their extensive infrastructure projects and increasing housing developments. The adoption of sustainable building practices and regulatory incentives for using industrial byproducts, including flue-gas desulfurization byproducts, further supports the region's anticipated dominance. Additionally, the rising urbanization is expanding the synthetic gypsum market in the region. For instance, a report published by the Asian Development Bank suggests that 55% of the population of Asia will be urban by 2030.

Source: Polaris Market Research Analysis

Curious About Regional Market Performance? Request Customization

Key Players and Competitive Insights

Prominent market players are investing heavily in research and development to expand their offerings, which drives the synthetic gypsum market growth. Market participants are also undertaking a variety of strategic activities to expand their global footprint, with important market developments including innovative launches, international collaborations, higher investments, and mergers and acquisitions between organizations. To expand and survive in a more competitive and rising market environment, the synthetic gypsum industry must offer innovative solutions.

The synthetic gypsum market is fragmented, with the presence of numerous global and regional market players. The players are leveraging extensive resources and customer bases to enhance the capabilities of the material. Knauf Group; HOLCIM; Saint-Gobain S.A.; National Gypsum Services Company; James Hardie Industries plc.; Georgia-Pacific; Etex Group; Synthetic Materials; YOSHINO GYPSUM CO., LTD; American Gypsum Company, LLC; and Beneficial Reuse Management are among the major synthetic gypsum market players.

Knauf Group, founded in 1932 by brothers Alfons and Karl Knauf, is a prominent multinational company based in Iphofen, Germany, specializing in building materials and construction systems. Knauf is also involved in the production and use of synthetic gypsum, which is utilized in various applications such as drywall, plasters, and cement products. In August 2023, Knauf started an upgrade at its Iphofen gypsum wallboard plant to switch its use of synthetic gypsum to natural gypsum.

Yoshino Gypsum Co., Ltd., founded in 1937 and headquartered in Tokyo, Japan, provides noncombustible building materials with a focus on solutions for sick building syndrome and interior plasterboard products. In May 2023, the company developed a new gypsum wallboard fixing method called ‘Smart JG’ that uses adhesive and a magnet. It is intended to replace the usual installation method using power tools, screws, and nails.

Key Companies

- Knauf Group

- HOLCIM

- Saint-Gobain S.A.

- National Gypsum Services Company

- James Hardie Industries plc.

- Georgia-Pacific

- Etex Group

- Synthetic Materials

- YOSHINO GYPSUM CO., LTD

- American Gypsum Company, LLC

- Beneficial Reuse Management

Synthetic Gypsum Industry Developments

- In April 2025: new research identified synthetic gypsum as a sustainable substitute for mined gypsum, emphasizing its high-value applications. Generated mainly as a byproduct of processes such as flue gas desulfurization, it is increasingly processed into advanced materials.

- In July 2025: a study published in Nature Scientific Reports analyzed the acoustic performance of gypsum-based composites produced from waste materials to promote environmental sustainability and effective noise control.

- December 2023: Etex Group, a global building material manufacturer, acquired BGC's gypsum and fiber cement operations in Australia, including wallboard, plaster, compound, and cornice production facilities.

- November 2023: Beneficial Reuse Management (BRM), a major provider of beneficial reuse solutions for non-hazardous reusable waste streams, announced the acquisition of USA Gypsum, LLC (USAG), based in Denver, PA. The acquisition gives BRM an opportunity to diversify gypsum sources to grow its geographic footprint.

- October 2023: Saint-Gobain S.A., a construction and building products manufacturing company, announced that it had acquired the remaining equity interest and assets of Seven Hills Paperboard LLC, including a gypsum paper board liner manufacturing facility in Lynchburg, Virginia.

Market Segmentation

By Type Outlook (Revenue, USD million, 2019–2032)

- Flue Gas Desulfurization (FGD) Gypsum

- Fluorogypsum

- Phosphogypsum

- Titanogypsum

- Others

By Application Outlook (Revenue, USD million, 2019–2032)

- Cement

- Gypsum Board

- Soil Amendments

- Dental

- Other

By End-User Industry Outlook (Revenue, USD million, 2019–2032)

- Construction Industry

- Agriculture Industry

- Other

By Regional Outlook (Revenue, USD million, 2019–2032)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- South Korea

- Indonesia

- Australia

- Rest of Asia Pacific

- Middle East & Africa

- Saudi Arabia

- UAE

- Israel

- South Africa

- Rest of Middle East & Africa

- Latin America

- Mexico

- Brazil

- Argentina

- Rest of Latin America

Report Scope

| Report Attributes | Details |

| Market Size Value in 2023 | USD 1,310.40 million |

| Market Size Value in 2024 | USD 1,364.25 million |

| Revenue Forecast in 2032 | USD 1,895.08 million |

| CAGR | 4.2% from 2024 to 2032 |

| Base Year | 2023 |

| Historical Data | 2019–2022 |

| Forecast Period | 2024–2032 |

| Quantitative Units | Revenue in USD million and CAGR from 2024 to 2032 |

| Report Coverage | Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

| Segments Covered |

|

| Regional Scope |

|

| Competitive Landscape |

|

| Report Format |

|

| Customization | Report customization as per your requirements with respect to countries, regions, and segmentation. |

Source: Polaris Market Research Analysis

Synthetic Gypsum Market FAQ's

The global synthetic gypsum market size was valued at USD 1,310.40 million in 2023 and is projected to grow to USD 1,895.08 million by 2032.

The global market is projected to record a CAGR of 4.2% during the forecast period.

North America had the largest share of the global market in 2023.

Key players in the market are Knauf Group; HOLCIM; Saint-Gobain S.A.; National Gypsum Services Company; James Hardie Industries plc.; Georgia-Pacific; Etex Group; Synthetic Materials; YOSHINO GYPSUM CO., LTD; American Gypsum Company, LLC; and Beneficial Reuse Management.

The flue gas desulfurization (FGD) gypsum type segment is projected for significant growth in the global market during the forecast period.

The cement segment dominated the market in 2023.

Download Sample Report of Synthetic Gypsum Market

Please fill out the form to request a customized copy of the research report.