What is the Current Market Size?

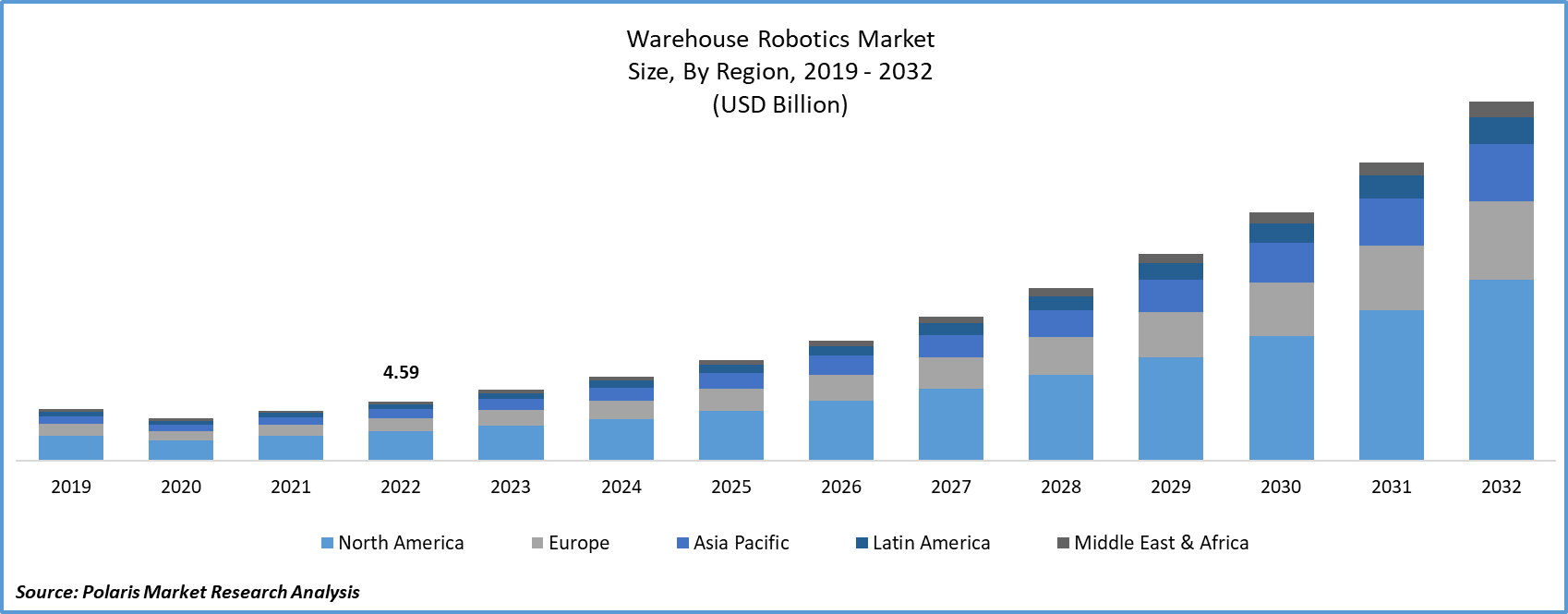

The global warehouse robotics market was valued at USD 6.48 billion in 2024 and is expected to grow at a CAGR of 19.74% during the forecast period. Key factors driving the demand includes amplification of e-commerce industry, enlarged focus on effective and efficient software solutions, and rising use of IIoT technology in robotics.

Key Insights

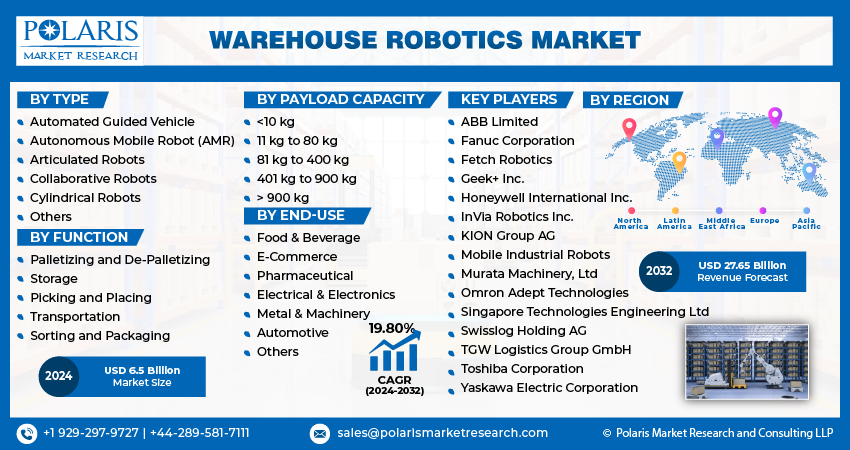

- In 2024, the automated guided vehicles segment held the largest share. This is due to their use in the transportation of goods, which reduces logistics costs and optimizing supply chains.

- The storage segment dominated the market in 2024. This is due to automation in inventory management, reduced labor costs, and improved safety.

- Asia Pacific dominated the market in 2024 attributed to the rise in warehouse automation, which drives the adoption and investments in these technologies.

- North America is expected to witness the fastest growth during the forecast period. This is due to the e-commerce expansion, advances in technology, and labor shortages.

Industry Dynamics

- The growth of e-commerce is driven by online shopping, which results in large inventories and complex warehouse storage, thereby boosting demand.

- The rise in investment for warehouse robotics enables efficiency, fast delivery, and safety in management, driving the adoption of robotics.

- The integration of technologies requires high initial investments, which creates a barrier to adoption, especially for small-scale businesses.

- The growth of e-commerce creates opportunities for efficiently expanding automated solutions for order fulfillment.

Market Statistics

- 2024 Market Size: USD 6.48 billion

- 2034 Projected Market Size: USD 39.14 billion

- CAGR (2025-2034): 39.14%

- Asia Pacific: Largest market in 2024

AI Impact on the Industry?

- Enhance complex decision-making and navigation of robot intelligence.

- Inventory placement and warehouse optimization for maximum efficiency.

- Reduction in downtime and operational cost enables predictive maintenance.

- Creates safe and flexible workflows to facilitate human-robot collaboration.

What Does the Current Market Landscape Look for Warehouse Robotics?

Warehouse robotics represents a computer-driven approach employed to efficiently manage material transport while optimizing and automating various warehouse operations. This innovative system relies on dedicated machinery and software solutions for tasks such as item retrieval and placement, packing, material transportation, packaging, and palletization, all executed with remarkable precision. Warehouse robotics encompasses a range of technologies, including industrial robots, sorting mechanisms, conveyors, autonomous mobile robots (AMR), and automated storage and retrieval systems (AS/RS).

To Understand More About this Research: Request a Free Sample Report

Warehouse operations have been revolutionized by the use of robotic systems. These systems use computer systems, onboard sensors, magnetic strips, infrared cameras, and maps to navigate, avoid obstacles, and transport inventory. By taking over repetitive tasks, these robots reduce workload on human workers and remain resilient against fatigue and wear and tear. Warehouse robotics are now indispensable in sectors such as food and beverage, automotive, pharmaceutical, and retail. For instance, Walmart and Symbiotic have collaborated to introduce cutting-edge automation into their supply chain. The robotic systems deployed in their warehouses excel at sorting, retrieving, storing, and packing goods with remarkable precision. This enhances the efficiency of the intake process, leading to faster operations, and improves the accuracy of inventory storage for subsequent orders.

Warehouses serve as essential hubs for storage and distribution in various industries. Many prominent corporations operate vast warehouse facilities that encompass both vertical and horizontal storage capacities. Given their intricate nature, automation is instrumental in enhancing operational efficiency, resulting in significant time and cost savings. Warehouse robots, renowned for their precision and efficiency surpassing human labor, are increasingly deployed based on their specific utility.

The adoption of warehouse robotics accelerated as companies sought to automate their operations and reduce human contact in their facilities. This surge in demand for robotics solutions has led to increased investments in research and development, resulting in more advanced and efficient robotics technology.

Moreover, the pandemic has highlighted the importance of supply chain resilience, prompting many businesses to reevaluate their logistics strategies and invest in robotics to enhance their operational flexibility. As a result, the warehouse robotics market has witnessed robust growth during and after the pandemic, with a promising outlook for the future.

The global warehouse robotics market is experiencing a boost due to the rising use of IIoT technology in robotics. Industrial robots are now fitted with IIoT devices, such as smart sensors, which gather data and improve productivity. IIoT systems, which consist of smart devices, data infrastructure, and cloud-based analytics, provide valuable insights for informed decision-making. The data collected from IoT systems and sensors in production, including warehouse robotics, aids in analyzing manufacturing efficiency, enhancing asset reliability, and improving cost efficiency.

Industry Dynamics

Growth Drivers

What are the Factors Driving the Expansion Opportunities?

The e-commerce industry has seen remarkable growth in recent years, primarily due to factors such as mobile adaptability, omnichannel retailing, improved convenience for both buyers and sellers and a broader range of product offerings from various brands. The increasing preference of customers for online shopping has led to a surge in inventory stored in company warehouses. To meet this rising consumer demand, companies need to expand their product range, all while ensuring the safe storage and packaging of these items.

However, as the volumes of goods increase, managing storage and packaging operations becomes increasingly challenging. Companies have been actively investing in tools that offer quick returns on investment and higher efficiency to streamline their warehouse operations and reduce delivery times. This has led to the widespread adoption of warehouse robotics solutions in company warehouses. These warehouse robotics solutions are gaining popularity as comprehensive answers to efficiently handle order management and fulfillment processes in the e-commerce sector. Additionally, they enhance human safety, facilitate flexible material movement, and provide traceability.

Report Segmentation

The market is primarily segmented based on type, function, payload capacity, end-use, and region.

|

By Type |

By Function |

By Payload Capacity |

By End-Use |

By Region |

|

|

|

|

|

To Understand the Scope of this Report: Speak to Analyst

Segment Insights

Type Analysis

Which Segment by Type Held the Largest Revenue Share?

The Automated Guided Vehicle (AGV) segment held the largest revenue share in 2024. The primary use of warehouse roots lies in the transportation of items within warehouses and storage facilities through mobile automated guided vehicles (AGVs). These robots are responsible for moving goods along predetermined routes, facilitating their storage and shipment. AGVs play a pivotal role in reducing logistical expenses and optimizing supply chain operations. Moreover, AGVs are employed in the processes of item selection and replenishment, both during inbound and outbound handling. What distinguishes autonomous mobile robots from AGVs is the extent of autonomy they possess.

Function Analysis

Why Storage Segment dominated the Market in 2024?

The storage segment dominated the market in 2024. Effective storage solutions are an indispensable component of contemporary warehouse automation. Employing automated storage systems, prevalent in modern warehouses, enhances organizational efficiency by providing users with improved inventory management, control, and tracking capabilities. Furthermore, these solutions contribute to heightened workplace safety, simultaneously reducing labor costs and the requisite workforce. Anticipated to surge in tandem with increasing manufacturing activity, the ascent of technologies like Industry 4.0 in manufacturing facilities, and the expansive growth of the global transportation and logistics market, the utilization of warehouse robots is on the rise.

Regional Insights

Which Region Accounted for the Largest Share of the Global Market?

Asia-Pacific dominated the market share in 2024 due to the increasing investments in the sector, the manufacturing industry is poised to secure a substantial market share and become a significant player in the region. Chinese businesses that had previously deployed these robots in their warehouses experienced positive outcomes during times of crisis. JD.com, a major Chinese e-commerce company headquartered in Wuhan, operates automated warehouses equipped with a fleet of robotic trucks. These robots facilitate the delivery of essential goods to urban customers who prefer online shopping and may be confined to their homes.

What are the Factors Driving the Growth of North America?

North America is anticipated to grow fastest over the forecast period. The proliferation of e-commerce, coupled with advancements in technology enhancing the capabilities of robots, cost reduction, and labor shortages in specific industries, are the key factors driving the rising utilization of robots within North American warehouses and distribution centers. Many businesses across North America are collaborating with tech firms to jointly develop robots for potential deployment in retail outlets, aimed at assisting customers in finding desired products and accessing additional information, like interactive product displays and research resources.

Key Market Players & Competitive Insights

The market is characterized by intense competition, with established players relying on advanced technology, high-quality products, and a strong brand image to drive revenue growth. These companies employ various strategies such as research and development, mergers and acquisitions, and technological innovations to expand their product portfolios and maintain a competitive edge in the market.

Some of the major players operating in the global market include:

- ABB Limited

- Fanuc Corporation

- Fetch Robotics

- Geek+ Inc.

- Honeywell International Inc.

- InVia Robotics Inc.

- KION Group AG

- Mobile Industrial Robots

- Murata Machinery, Ltd

- Omron Adept Technologies

- Singapore Technologies Engineering Ltd

- Swisslog Holding AG

- TGW Logistics Group GmbH

- Toshiba Corporation

- Yaskawa Electric Corporation

Recent Developments

- September 2025,Dyna Robotics secured USD 120 million in Series B funding led by Nvidia and Amazon, accelerating AI-driven manipulation systems. Source: https://www.mordorintelligence.com/industry-reports/warehouse-robotics-market

- In December 2022, ABB unveiled the "ABB SWIFT CRB 1300" collaborative robot designed to automate diverse warehouse tasks, including palletizing and pick-and-place operations. This introduction empowers ABB's clientele to enhance process flexibility, efficiency, and resilience through robotic automation. By deploying this technology, ABB customers can address labor shortages by allowing their workforce to focus on essential business activities.

- In September 2022, Honeywell introduced its latest robotic innovation, the "Smart Flexible Depalletizer," aimed at enhancing warehouse productivity through the reduction of manual labor.

- In August 2022, Yaskawa introduced a collaborative robot with machine vision capabilities known as the MOTOMAN-HC30PL. This robot is designed for palletizing applications and can handle payloads of up to 30 kilograms.

Warehouse Robotics Market Report Scope

|

Report Attributes |

Details |

|

Market size value in 2024 |

USD 6.48 billion |

| Market size value in 2025 | USD 7.73 billion |

|

Revenue forecast in 2034 |

USD 39.14 billion |

|

CAGR |

19.74% from 2025 – 2034 |

|

Base year |

2024 |

|

Historical data |

2020 – 2023 |

|

Forecast period |

2025 – 2034 |

|

Quantitative units |

Revenue in USD million/billion and CAGR from 2025 to 2034 |

|

Segments Covered |

By Type, By Function, By Payload Capacity, By End-Use, By Region |

|

Regional scope |

North America, Europe, Asia Pacific, Latin America; Middle East & Africa |

|

Customization |

Report customization as per your requirements with respect to countries, region and segmentation |

Want to check out the warehouse robotics market report before buying it? Then, our sample report has got you covered. It includes key market data points, ranging from trend analyses to industry estimates and forecasts. See for yourself by downloading the sample report.

FAQ's

• The global market size was valued at USD 6.48 billion in 2024 and is projected to grow to USD 39.14 billion by 2034.

• The global market is projected to register a CAGR of 19.74% during the forecast period.

• Asia Pacific dominated the market in 2024.

• A few of the key players in the market are ABB Limited; Fanuc Corporation; Fetch Robotics; Geek+ Inc.; Honeywell International Inc.; InVia Robotics Inc.; KION Group AG; Mobile Industrial Robots; Murata Machinery, Ltd; Omron Adept Technologies; Singapore Technologies Engineering Ltd; Swisslog Holding AG; TGW Logistics Group GmbH; Toshiba Corporation; and Yaskawa Electric Corporation.

• In 2024, the automated guided vehicles segment held the largest share.

• The storage segment dominated the market in 2024.

Page last updated on:

Nov-2023

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements