Market Overview

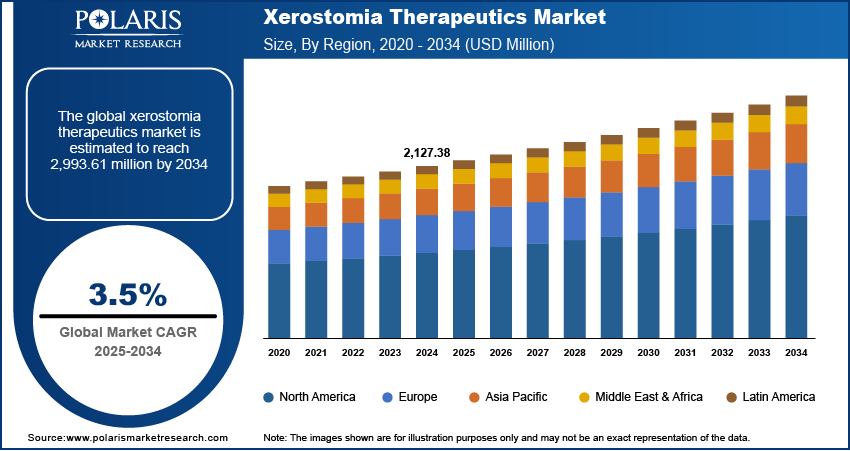

The xerostomia therapeutics market size was valued at USD 2.31 billion in 2025. The market is projected to exhibit a CAGR of 4.1% during 2026–2034.

The xerostomia therapeutics market focuses on treatments for dry mouth. It is a condition caused by reduced saliva production due to various factors. It includes medication use, radiation therapy, autoimmune diseases, and aging. The market is fueled by the increasing prevalence of chronic diseases, the rising elderly population, and growing awareness of the condition’s impact on oral health. Key xerostomia therapeutics market trends include advancements in saliva substitutes, the development of novel drug formulations, and increased research into regenerative therapies that target salivary gland function. Also, pharmaceutical companies are investing in prescription treatments. Over-the-counter (OTC) product availability continues to expand and this drives market growth.

The market is served by a combination of over-the-counter (OTC) xerostomia products, which offer symptomatic relief, and prescription sialogogues, which are used for more serious cases. The market is also benefiting from innovation, such as longer-lasting oral moisturizer gel, tele-dentistry access models, and regenerative treatments for salivary gland dysfunction. For manufacturers and investors, the key to growth in the category will be the strength of the distribution network, both in retail and online, the breadth of the category’s use in dental and oncology care, and product differentiation in formulation, format, and longer-lasting relief.

Key Dynamics

-

The OTC segment accounted for a significant share of the xerostomia therapeutics market in 2025. OTC products are generaly preferred due to their easy availability and symptomatic relief from dry mouth. Patients usually require sprays, gels, lozenges, and rinses for symptomatic treatment.

-

The saivary stimulants segment held a major share of the market. These products help activate residual salivary gland function. They provide ease for patients experiencing dry mouth condition.

-

North America recorded the argest regional share in 2025. High commonness of dry mouth-related conditions, strong awareness initiatives, and well-developed healthcare systems support the regional market growth.

-

The Asia Pacific region is expected to witness the fastest growth during the forecast period. Increasing research activities, broadening heathcare infrastructure, and rising prevalence of chronic diseases are driving regional market growth.

Industry Dynamics

-

Growing avaiability of OTC dry mouth products is supporting market development. Retail pharmacies, online pharmacies, and e-commerce platforms provide easy access to saliva substitutes and oral moisturizers.

-

Product innovation is increasing within the xerostomia therapeutics market. Companies are deveoping improved sprays, gels, rinses, and lozenges. These products provide longer-lasting ease and more patient comfort.

-

Growing focus on personaized care and diagnostics is expected to create several market opportunities.

-

High costs of branded prescription siaogogues may hinder market growth.

Market Statistics

-

2025 Market Size: USD 2.31 billion

-

2034 Projected Market Size: USD 3.32 billion

-

CAGR (2026–2034): 4.1%

-

North America: Largest market in 2025

Market Dynamics

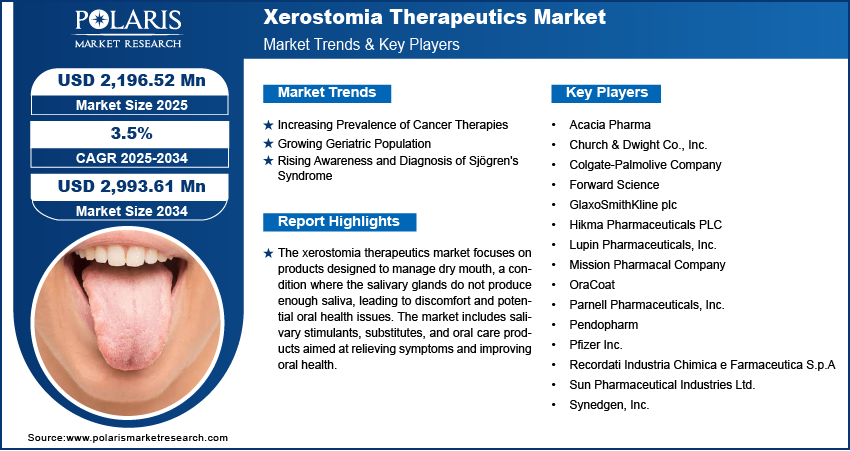

Increasing Prevalance of Cancer Therapies

The rising adoption of chemotherapy and radiotherapy in cancer treatment has led to a higher incidence of xerostomia among patients. These therapies often damage salivary glands. Saliva production is reduced during treatment. This increase in chemotherapy and radiotherapy propels the xerostomia therapeutics market demand.

Radiation-induced xerostomia (RIX) often requires multi-product management. This management is implemented using moisturizers, saliva substitutes, and dental hygiene adjuncts. As patients need ongoing relief, the demand for purchase is boosted. It also strengthens the need for clinically positioned solutions. Oncology clinics play a key role in integrating these into care pathways. This helps cancer patients manage dry mouth symptoms effectively over time.

To Understand More About this Research:Request a Free Sample Report

Growing Geriatric Population

The expanding older adult population contributes hugely to the xerostomia therapeutics market growth. According to the World Health Organization, the global population aged 60 years and above is expected to reach 2.1 billion by 2050, up from 900 million in 2015. Aging is associated with a natural decline in salivary gland function and an increase in chronic diseases. The medications for these chronic diseases may induce dry mouth as a side effect. This directly leads to a high demand for xerostomia therapeutics.

Medication-induced xerostomia from polypharmacy is a major issue in aging groups. Managing chronic diseases raises the use of chronic disease medications linked to dry mouth symptoms. This supports demand for accessible OTC xerostomia relief options and physician-recommended dry mouth products. These help older adults handle side effects simply while continuing their regular treatments without hassle.

Increasing Awareness and Diagnosis of Sjögren's Syndrome

Patients diagnosed with Sjögren's syndrome experience extreme dry mouth. This affects their ability to speak, eat, and maintain oral health. Healthcare experts across the world are educating patients about this condition. They are emphasizing the importance of early intervention, thereby boosting demand for xerostomia therapeutics.

Market Restraints

Xerostomia treatment challenges arise from a variable response to saliva substitutes and their short duration of relief. Adherence issues from frequent dosing and xerostomia drug side effects concern patients using prescription options. In OTC-heavy categories, OTC competition and price pressures push brands toward xerostomia product innovation. The products include sprays and gels. Dental partnerships and telehealth channels help provide better reach.

Segment Insights

By Type Insights

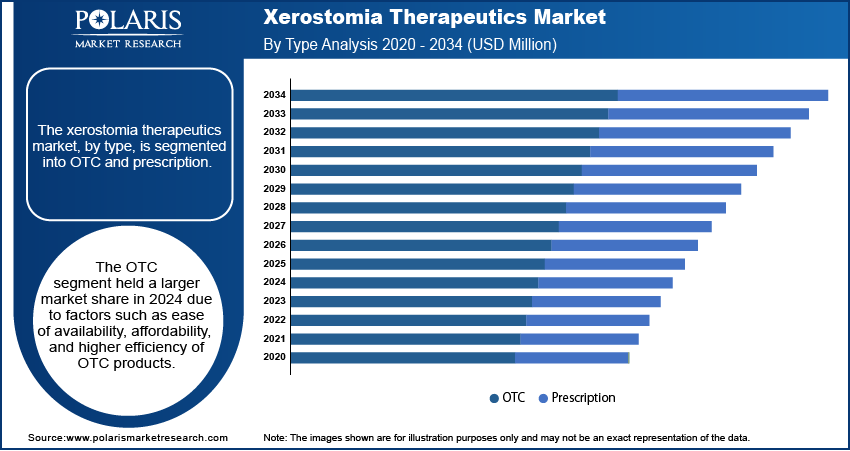

The xerostomia therapeutics market, by type, is segmented into OTC and prescription. The OTC segment dominated the market share in 2025. This dominance is attributed to factors such as ease of availability, affordability, and higher efficiency of OTC products. Patients usually prefer OTC solutions for immediate relief from dry mouth symptoms. This contributes to the segment's leading market position.

The prescription segment is experiencing significant growth. The growth of the the segment is driven by the growing frequency of chronic conditions such as Sjögren's syndrome and the side effects of certain medications that cause dry mouth. Healthcare professionals are prescribing targeted therapeutics to manage severe xerostomia cases. This leads to a rise in demand for xerostomia therapeutics within this segment.

By Product Insights

The xerostomia therapeutics market, by product, is segmented into salivary stimulants, salivary substitutes, and dentifrices. The salivary stimulants segment dominated the xerostomia therapeutics market in 2025. This share is due to their ability to activate residual salivary gland function, which helps relieve patients experiencing dry mouth. Salivary substitutes also play an essential role in managing xerostomia. They are particularly useful for individuals with limited or no salivary gland activity. These products include artificial saliva formulations. They help retain oral moisture and comfort. The usage of xerostomia therapeutics is essential for comprehensive xerostomia management, especially for patients undergoing treatments that weaken salivary function.

By Distribution Channel Insights

Based on distribution channel, the market is segmented into retail pharmacies, online pharmacies/e-commerce, and hospital/clinic dispensing. Demand grows through retail pharmacies with high Over-the-counter (OTC) output for dry mouth medicines. Online pharmacies and e-commerce offer an easy platform for saliva substitutes and subscription refills. Hospital pharmacies in oncology settings support incorporated xerostomia care. These channels meet varied patient needs effectively.

By Product Form Insights

By product form, the market is segmented into sprays, gels, rinses/mouthwashes, and lozenges. Factors like duration of relief, portability, taste, and usage frequency drive repeat buys and loyalty. Patients seek long-lasting dry mouth relief options that fit their daily routines easily.

By End User Insights

By end user, the market is segmented into dental clinics, hospitals and oncology centers, and homecare settings. Dental clinics lead for oral health maintenance and caries prevention advice. Hospitals and oncology centers use it to handle radiation cases. Homecare dry mouth treatment supports ongoing needs for chronic symptoms. These settings ensure targeted xerostomia oral health support.

By Application Insights

By application, the market is segmented into radiation-induced xerostomia (RIX), Sjögren’s syndrome-related xerostomia, and medication-induced xerostomia. Radiation-induced xerostomia (RIX) drives demand in oncology with multi-product xerostomia regimens. Sjögren’s xerostomia needs ongoing care for autoimmune cases. Medication-induced xerostomia from polypharmacy dry mouth supports OTC-first options. Each application shapes unique purchasing patterns. Oncology often bundles products, while medication cases start with OTC-first management.

Regional Outlook

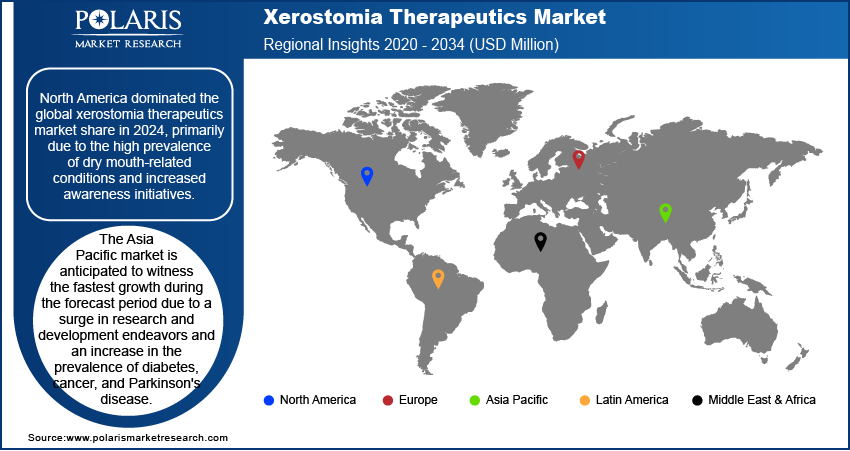

By region, the study provides xerostomia therapeutics market insights into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. North America dominated the xerostomia therapeutics market revenue share in 2025. This share is primarily due to the high commonness of dry mouth-related conditions and strong awareness initiatives in North America. The region's high revenue share is further backed by a significant number of patients looking for treatment, contributing to the North America xerostomia therapeutics market expansion.

High OTC penetration, strong dental care utilization, and mature retail plus e-commerce oral care channels drive steady sales. Oncology supportive care pathways keep demand strong for clinical solutions. Patients visit dentists often, boosting awareness and purchases. All these factors contribute to the region’s leading market position.

In Europe, the xerostomia therapeutics market is experiencing growth due to an increasing elderly population and high awareness of dry mouth conditions. The rising prevalence of diseases such as Sjögren's syndrome and rheumatoid arthritis contributes to the demand for effective treatments in the region. Additionally, initiatives aimed at raising awareness about dry mouth conditions are supporting the Europe xerostomia therapeutics market expansion.

The Asia Pacific xerostomia therapeutics market is anticipated to witness the fastest growth during the forecast period. Factors such as a surge in research and development endeavors, an increase in the prevalence of diabetes, cancer, and Parkinson's disease treatment, and growing collaborations among market participants are driving this expansion. The Japan xerostomia therapeutics market is expected to register the highest CAGR in the regional market during the forecast period, reflecting the region's significant market potential.

Asia Pacific sees strong growth due to pharmacy expansion and rising digital health adoption. Increasing awareness of oral health quality of life gains supports demand in the aging population in Asian countries. Better access to treatments and online health tools helps older adults manage dry mouth effectively. These trends fuel a consistent market rise across the region.

Key Players and Competitive Analysis

The xerostomia therapeutics market comprises several active companies offering various treatments for dry mouth. A few notable participants include GlaxoSmithKline plc, known for its product Biotène; Church & Dwight Co., Inc.; Colgate-Palmolive Company; Hikma Pharmaceuticals PLC; and Pendopharm. These companies provide a range of over-the-counter and prescription products aimed at alleviating xerostomia symptoms.

Other significant contributors to the market are Sun Pharmaceutical Industries Ltd.; Lupin Pharmaceuticals, Inc.; Pfizer Inc.; Parnell Pharmaceuticals, Inc.; and Acacia Pharma. These organizations focus on developing and distributing therapeutic solutions. Therefore, patients can manage dry mouth conditions with diverse medications as per their needs.

Companies such as OraCoat; Synedgen, Inc.; Recordati Industria Chimica e Farmaceutica S.p.A; Forward Science; and Mission Pharmacal Company are active in this industry. Their involvement enhances the availability of various treatment options. These companies are contributing to the overall growth and competitiveness of the xerostomia therapeutics market.

GlaxoSmithKline plc (GSK) is a major British multinational pharmaceutical and biotechnology company. The headquarters is located in Brentford, UK. GSK was established in 2000 through the merger of Glaxo Wellcome and SmithKline Beecham. The company manages operations globally. They have their research centers in the UK, USA, Belgium, and China. The company specializes in developing and marketing vaccines, pharmaceuticals, consumer healthcare products, and over-the-counter (OTC) medicines. It has a diverse portfolio. It includes treatments for respiratory diseases, HIV, cancer, cardiovascular conditions, and central nervous system disorders. GSK also offers vaccines for hepatitis A and B, whooping cough, and the world's first malaria vaccine (RTS, S). The company is renowned for its contributions to global health. They provide several essential medicines listed by the World Health Organization (WHO).

Acacia Pharma Group plc, founded in 2006 and is headquartered in Cambridge, United Kingdom. This is a biopharmaceutical company specializing in supportive care solutions. Patients who are undergoing surgery, invasive procedures, or chemotherapy get help via Acacia Pharma Group. The company operates as a subsidiary of Eagle Pharmaceuticals, Inc. Acacia Pharma’s portfolio includes FDA-approved products. The products include BARHEMSYS and BYFAVO. BARHEMSYS is an intravenous amisulpride for the treatment and prevention of postoperative nausea and vomiting (PONV). BYFAVO is an intravenous remimazolam used for procedural sedation during short medical interventions like colonoscopy. Additionally, the company has developed APD403, a selective dopamine antagonist amisulpride that has completed Phase II trials for chemotherapy-induced nausea and vomiting (CINV). Acacia Pharma’s innovative approach leverages known pharmaceuticals to develop rapid clinical proof-of-concept products tailored to unmet medical needs. Acacia Pharma has also explored xerostomia therapeutics through its product APD515. This treatment targets xerostomia in advanced cancer patients, focusing on improving their quality of life.

Competitive View

OTC oral care brands compete in a variety of formats. The variety of products offered includes sprays, gels, and rinses, along with an enhanced sensory experience. Prescription xerostomia drug players compete on clinical positioning for moderate to severe cases to achieve physician adoption. Specialty xerostomia solution players compete on strong clinical claims, dental support, and telehealth dental partnerships. Benchmarking different companies operating in the xerostomia market indicates that each company is catering to the needs of patients and treatments appropriately.

List of Key Companies

-

Church & Dwight Co., Inc.

-

Cogate-Palmolive Company

-

Forward Science

-

Hikma Pharmaceuticas PLC

-

Lupin Pharmaceuticas, Inc.

-

Mission Pharmaca Company

-

OraCoat

-

Parnel Pharmaceuticals, Inc.

-

Pendopharm

-

Pfizer Inc.

-

Recordati Industria Chimica e Farmaceutica S.p.A

-

Sun Pharmaceutica Industries Ltd.

-

Synedgen, Inc.

Industry Developments

- November 2025: Aquoral collaborated with Dentulu to broaden access to advanced xerostomia treatments through Dentulu’s telehealth network. This partnership aims to improve remote patient care and therapy delivery.

- October 2025: Researchers at the University of California, San Francisco, reported new advancements under the Hive Research initiative. The university highlighted progress in regenerative salivary therapies supported by SBIR grant funding.

- December 2024: MeiraGTx announced that the FDA granted Regenerative Medicine Advanced Therapy (RMAT) designation to AAV2-hAQP1 for the treatment of Grade 2/3 radiation-induced xerostomia (RIX).

Market Segmentation

By Type Outlook (Revenue – USD Billion, 2021–2034)

-

OTC

-

Prescription

By Product Outlook (Revenue – USD Billion, 2021–2034)

-

Saivary Stimulants

-

Saivary Substitutes

-

Dentifrices

By Distribution Channel Outlook (Revenue – USD Billion, 2021–2034)

-

Retai Pharmacies

-

Onine Pharmacies/E-Commerce

-

Hospita/Clinic Dispensing

By Product Form Outlook (Revenue – USD Billion, 2021–2034)

-

Sprays

-

Ges

-

Rinses/Mouthwashes

-

Lozenges

By Application Outlook (Revenue – USD Billion, 2021–2034)

-

Radiation-Induced Xerostomia (RIX)

-

Sjögren’s Syndrome-Reated Xerostomia

-

Medication-Induced Xerostomia

By End User Outlook (Revenue – USD Billion, 2021–2034)

-

Denta Clinics

-

Hospitas and Oncology Centers

-

Homecare Settings

By Regional Outlook (Revenue – USD Billion, 2021–2034)

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Netherlands

- Russia

- Rest f Europe

- Asia Pacific

- China

- Japan

- India

- Malaysia

- Suth Korea

- Indnesia

- Australia

- Vietnam

- Rest of Asia Pacific

- Midde East & Africa

- Saudi Arabia

- UAE

- Israel

- Suth Africa

- Rest of Middle East & Africa

- Latin America

- Mexic

- Brazil

- Argentina

- Rest f Latin America

Xerostomia Therapeutics Report Scope

|

Report Attributes |

Details |

|

Market Size in 2025 |

USD 2.31 billion |

|

Market Size in 2026 |

USD 2.40 billion |

|

Revenue Forecast by 2034 |

USD 3.32 billion |

|

CAGR |

4.1% from 2026 to 2034 |

|

Base Year |

2025 |

|

Historical Data |

2021-2024 |

|

Forecast Period |

2026-2034 |

|

Quantitative Units |

Revenue in USD billion and CAGR from 2026-2034 |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

|

|

Regional Scope |

|

|

Competitive Landscape |

Xerostomia Therapeutics Industry Trends Analysis (2025) Company Profiles/Industry participants profiling includes company overview, financial information, product/service benchmarking, and recent developments

|

|

Report Format |

PDF + Excel |

|

Customization |

Report customization as per your requirements with respect to countries, regions, and segmentation.

|

How is the report valuable for an organization?

Workflow/Innovation Strategy

The xerostomia therapeutics market has been segmented into detailed segments of type, product, distribution channel, product form, application, and end user. Moreover, the study provides the reader with a detailed understanding of the different segments at both the global and regional levels.

Growth/Marketing Strategy

The xerostomia therapeutics market growth and marketing strategy focus on expanding product offerings. They also focus on increasing awareness about dry mouth conditions. Companies are investing in research and development to introduce innovative solutions. These solutions include advanced salivary substitutes and stimulants. They are important to address a broader range of patient needs. Collaborative partnerships, especially with healthcare experts, are being prioritized to improve diagnosis and treatment access. Additionally, companies are leveraging digital platforms for targeted marketing and expanding distribution channels, including online sales and pharmacies, to reach a wider audience. These strategies are aimed at capitalizing on the growing demand driven by an aging population and increasing awareness of xerostomia.

FAQ's

The xerostomia therapeutics market was valued at USD 2.31 billion in 2025. The market is expected to reach USD 3.32 billion by 2034. It is expected to register a CAGR of 4.1%.

The demand for oncology supportive care is increasing due to the prevalence of radiation-induced xerostomia (RIX), which is a side effect of chemotherapy and radiotherapy for cancer patients.

In mild-to-moderate xerostomia cases, saliva substitutes such as sprays and gels are commonly preferred for quick symptom relief.

Doctors recommend sialogogues when xerostomia symptoms are severe and OTC treatments do not provide enough relief.

Sprays, gels, rinses, and lozenges are gaining traction because they are easy to use and provide convenient dry mouth relief.

Medication-induced xerostomia from polypharmacy increases demand for OTC dry mouth products as patients look for simple daily relief.

North America leads the xerostomia therapeutics market.Asia Pacific grows fastest due to rising healthcare access and aging populations.

Key companies such as GlaxoSmithKline, Colgate-Palmolive, Pfizer, and Hikma Pharmaceuticals differentiate through product formats, wider distribution, and healthcare partnerships.Advancements in Product Formulations: Development of more effective and long-lasting salivary stimulants and substitutes to improve patient comfort. Increased Focus on Prescription Treatments: Growing demand for prescription drugs that target the root causes of xerostomia, particularly in patients suffering from chronic conditions such as Sjögren's syndrome. Rise in Over-the-Counter Products: Expanding availability of OTC products offers convenience and affordability for individuals seeking quick relief. Use of Digital Platforms: Companies are utilizing e-commerce and digital marketing strategies to reach wider audiences and improve accessibility to treatments.

Page last updated on:

Oct-2023

Research Methodology

A robust system of research, verification, and forecasting designed to ensure reliable and actionable market insights.

Polaris Market Research uses a clear and structured approach to deliver insights that clients can rely on. The process combines detailed primary and secondary research, including direct communication with industry experts. The detailed information helps build a complete picture of market trends and developments. Secondary data is gathered from credible sources such as industry reports, company filings, government source links, and trusted organization databases. It is then cross-checked through discussions with key stakeholders across the value chain. Market size and forecasts are developed using both bottom-up and top-down methods to ensure accuracy and consistency in the final results.

Project Setup

Step 1 & 2:

- We start every project by clearly understanding the client’s objective or goal, then defining the market scope, and aligning regions, segments, and timelines.

- Once the foundation is set, we collect data from all-around of sources, including company reports, government databases, and paid industry platforms.

- Our research is based on secondary data, which helps us build a strong understanding of the market across regions and industries. Then we validate this information through primary research by speaking directly with industry experts, companies, and stakeholders.

- By combining secondary and primary research, we ensure that our market insights are accurate, practical, and closely aligned with real market conditions.

Data Collection

We gather information from both public and verified sources:

Data Structuring

Step 3:

- All collected data is organized into a consistent format to ensure accurate analysis. Since inputs come from multiple sources, they are standardized and aligned before use.

- The data is segmented by product, application, and region, and mapped across a defined historical period (2020–2024). All values are converted into common units (USD Mn/Bn), and volume and pricing are aligned where required to estimate revenue.

- Any overlaps or inconsistencies are reviewed and adjusted to maintain accuracy (<5% variance threshold).

- The result is a structured dataset that allows for clear comparison across regions and supports reliable analysis and forecasting.

Structured Market Dataset, USD Mn/Bn

4. Data Structuring

Step 4: TOP-DOWN APPROACH

- We start with the overall market size at a global or macro level.

- The market is then narrowed down based on scope and industry relevance.

- We apply penetration rates and split the data by region and segment.

- This helps us estimate the market size for specific segments.

- The numbers are validated through cross-checks to ensure accuracy.

Step 5: BOTTOM-UP APPROACH

- We begin by analyzing data from leading companies in the market.

- Revenue data is collected and mapped across different segments.

- The data is then aggregated to estimate the total market size.

- To fill in any gaps, adjustments are made based on industry standards.

- Validation checks make sure that the results are correct.

5. Data Structuring

Step 6:

At Polaris Market Research, we employ a methodical forecasting strategy. This approach blends the analysis of historical data with real-time market validation. To forecast future trends with precision, we examine past patterns, pricing fluctuations, and the interplay of supply and demand. To ensure our conclusions reflect the present market landscape, we actively seek input from industry experts and key stakeholders.

To refine our predictions, we carefully consider critical elements such as market drivers and restraints, fluctuations in raw material costs, emerging technologies, and the production capabilities of various regions. Furthermore, we assess regulatory frameworks and potential policy shifts to gauge their potential impact on market expansion.

All this information is synthesized to generate precise forecasts for each segment and region. These forecasts illuminate the current state of the market and highlight forthcoming opportunities.

6. Data Structuring

Step 7:

In the final stage, we validate all our estimates using a triangulation method, where data is cross-checked from multiple reliable sources, like company data, primary interviews, and secondary research. This helps us make sure that our numbers are correct and fit with the rest of the market.

This process involves verifying data consistency across various segments and geographic areas. It also requires comparing historical trends with the assumptions support the forecast. Any discrepancies involve adjustments to ensure everything remains aligned and dependable.

Once the data is finalized, we prepare the final outputs, including market size estimates, segment-wise breakdowns, and growth metrics. These are delivered in structured formats such as tables, charts, and data files for easy analysis and use.

We collaborate closely with clients, ensuring the final products align with their requirements. This includes offering tailored adjustments, supplementary data analyses, and continuous assistance. Furthermore, we monitor market trends post-delivery, providing updates and refinements to maintain the insights' relevance as time passes.

Post-delivery, we continue to monitor market shifts, offering updates and adjustments to ensure the insights remain relevant over time.

Validation

Triangulation Framework

- Company-level data

- Primary inputs from industry participants

- Secondary benchmarks and published data

- Variance maintained within ±5-10%

- Adjustments applied to align estimates

- Segment values validated against overall market structure

Quality Check

Data Consistency & Integrity

- Segment totals validated to 100%

- Regional estimates aligned with global market size

- Historical trends compared against forecast outputs

- Assumptions reviewed for cross-segment and regional alignment

Output & Delivery

Final Outputs

- Market size estimates (USD Mn/Bn)

- Segment-wise distribution (%)

- Growth metrics (CAGR %)

- Structured tables and charts

- Segment-level datasets

- Excel-based data files for further analysis

Client Alignment & Support

- Deliverables are aligned with defined client requirements and scope

- Custom data cuts and segment splits are incorporated as required

- Post-delivery queries are addressed through analyst interactions

- Additional clarifications and data support are provided upon request

Client Continuity & Updates

- Market developments are tracked post-delivery to capture changes in key trends

- Updated data and revisions are provided based on new market inputs

- Additional refinements and data cuts are shared as required

- Continued analyst engagement supports evolving client requirements